As the world entered a new decade at the start of 2020, it became clear that a new era of investing had arrived: one where technology, finances and a focus on creating a better future intersect.

From inception, Inyova’s mission has been to help develop this new model further. We believe in creating a more sustainable world through investing. And even though we’re a technology-focused company, we’re human at heart. This means that we aim to help every customer, regardless of where they are in life or in their investment journey. Whether that client is a complete newbie or an experienced investor, someone just heading to university or someone celebrating their retirement, we guide them in a way that serves both their financial goals and individual values.

But investment habits vary. In order to best serve our clients (and potential clients), we set out to gather broad data to gauge current Switzerland investing statistics. We kicked off 2020 by conducting a survey of more than 600 people — one of the biggest research projects ever done on investment habits in Switzerland.

In our survey, we asked questions relating to investment knowledge and experience, followed by questions regarding gender, age, pre-tax income, area of residency in Switzerland, years of working experience, and financial goals.

This investment research provides insight into trends, current client experience and financial goals.

Key takeaways from the survey results:

- 65% of women have never invested, as compared to 20% of men.

- Those with the primary financial goal of giving their family a more secure life are also less likely to have tried investing.

- Only 8% of investors use a traditional bank for their investments.

- 32% of those who have invested before set aside between CHF 500 and 1,000 each month for savings or investments.

- Those with more working experience tend to set aside less money for investments and are less likely to add money to current investments.

Keep reading for a deeper analysis of the survey results and potential implications for the future.

Note: the survey took place from mid-Feb to mid-March 2020, before the peak of the COVID-19 outbreak.

Investment knowledge and experience

We started with the following questions:

On a scale of 1-5, how do you rate your investment knowledge?

The average was 2.5.

How much investing experience do you have?

I have a little experience: 49 %

None – I’ve never invested: 44 %

I consider myself an experienced investor: 7 %

From here, only those who already had investing experience (i.e. who answered the second question with ‘I have a little experience’ or ‘I consider myself an experienced investor’) proceeded to the next part of the survey. For some questions, it was possible to choose more than one answer. It was also possible to skip questions. Out of the 603 people surveyed, 339 answered the following questions:

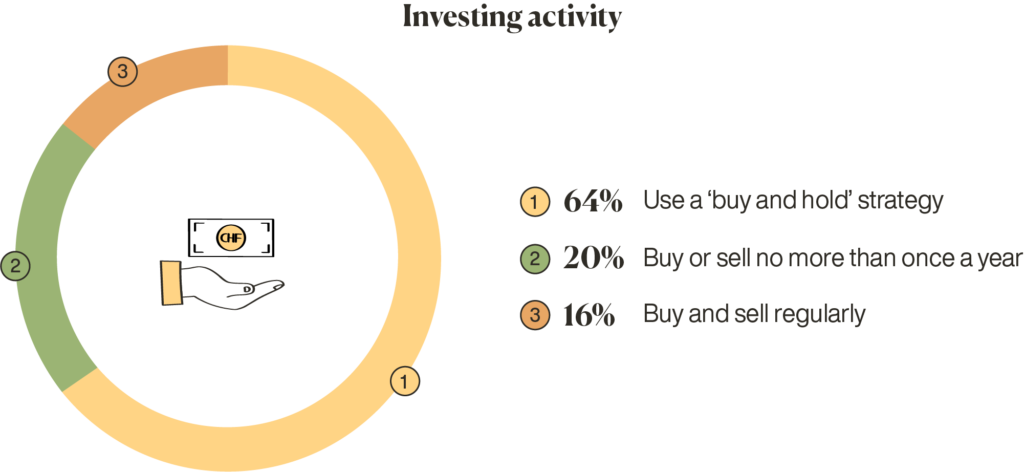

How active of an investor are you?

I buy and hold investments: 64%

I buy and sell no more than once a year: 20%

I regularly buy and sell investments: 16%

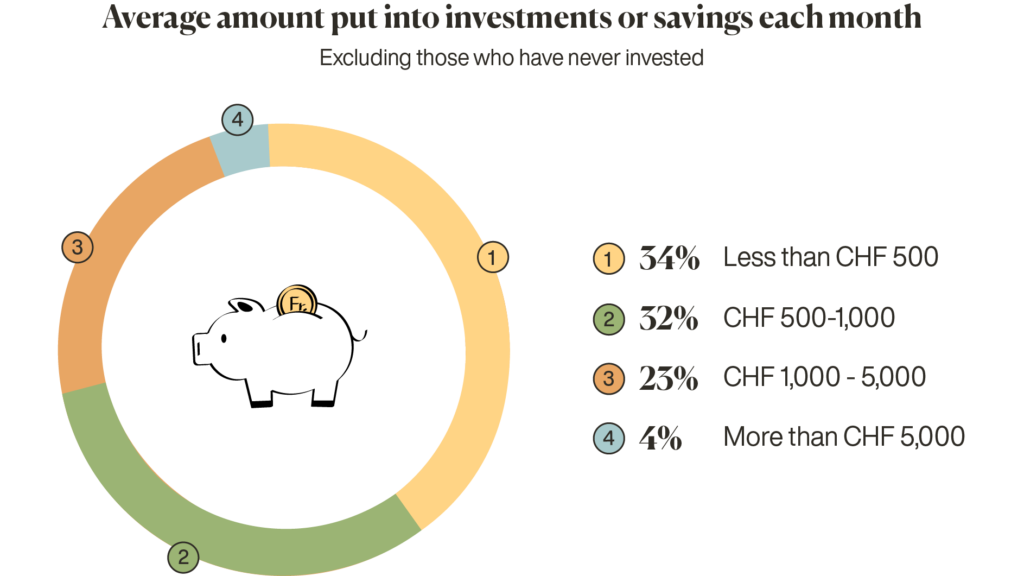

On average, how much money do you set aside each month for investments/savings?

Less than CHF 500: 34%

Between CHF 500 and 1,000: 32%

Between CHF 1,000 and 5,000: 23%

More than CHF 5,000: 4%

Who manages your investments?

I do so myself: 55%

A bank: 8%

An online advisor: 6%

A personal advisor: 6%

A combination: 24%

Are you planning to add more money to your investments within the next twelve months?

Yes: 87%

No: 12%

I am planning to withdraw money: 1%

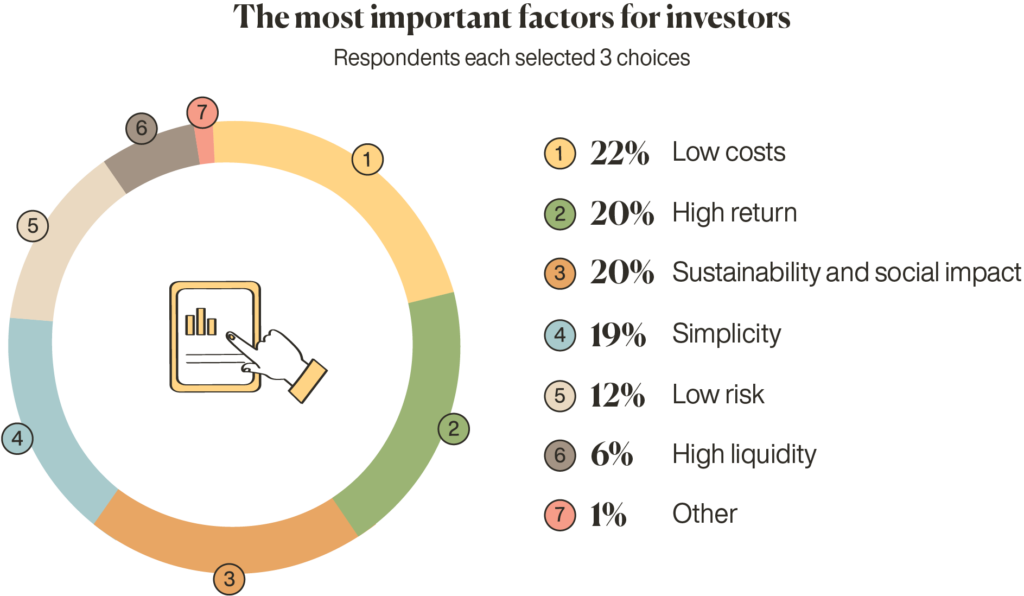

When investing, which three factors are the most important to you?

Low costs: 22%

High return: 20%

Sustainability and social impact: 20%

Simplicity: 19%

Low risk: 12%

High liquidity: 6%

Other: 1%

What investments do you currently have?

Pillar 3a/retirement accounts: 20%

Savings accounts: 20%

Stocks: 14%

EFTs: 13%

Cryptoassets: 7%

Real-estate investments: 7%

Investments in start-ups: 5%

Investments in gold/precious metals: 5%

Investments in bonds/fixed-term deposits: 5%

Investments in foreign exchange trading: 2%

Did your investments make money in 2019?

Yes, under 5%: 32%

Yes, between 5% and 10%: 31%

Yes between 10% and 25%: 14%

I don’t know, I haven’t checked: 13%

No, my returns were negative: 6%

Yes, over 25%: 4%

Next, the 264 people who had never invested rejoined the survey to answer the following question:

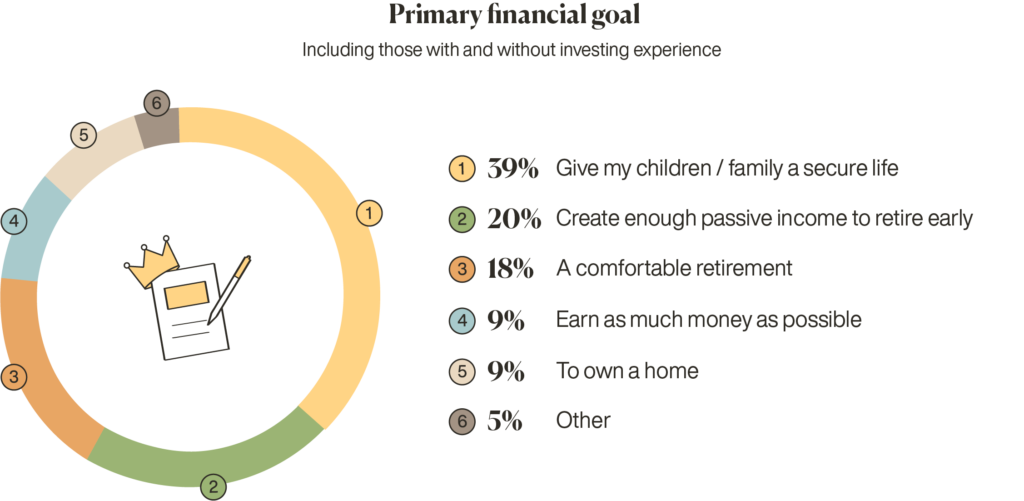

What is your number one financial goal?

To give my children/family a secure life: 39%

To create enough passive income to retire early: 20%

A comfortable retirement: 18%

To own a home: 9%

To earn as much money as possible: 9%

Other: 5%

Who is investing in Switzerland?

We will go into the demographic data in more detail later in this article. For now, let’s look at the specifics of Swiss investing habits. Let’s start by considering our main two groups: those with investment experience, and those without.

Those with investing experience

Out of the 603 people surveyed, 44% have never invested and 49% have a little experience. Only 7% of those surveyed consider themselves experienced investors.

source: Inyova

More than half (54%) of those with investing experience are aged between 30 and 49, and most have an annual pre-tax income above CHF 75,000.

- 34% earn less than CHF 75,000

- 22% earn CHF 75,000-99,999

- 32% earn more than CHF 100,000

- 12% preferred not to answer this question

Unsurprisingly, there was a direct correlation between investment experience and knowledge about investing. When asked ‘how do you rate your investment knowledge?’, those with a high level of experience rated their knowledge 3.2 out of 5 on average. Meanwhile, the group without experience rated their knowledge 1.6 out of 5 on average.

As for the amount of money set aside strictly for investment purposes, most participants invest less than CHF 1,000 each month.

source: Inyova

Additionally, 64% of the survey population are passive investors — they tend to ‘buy and hold’ as opposed to those who buy or sell regularly (16%). The top three investment choices are: Pillar 3a/retirement accounts (20%), savings accounts (20%), and the stock market (14%).

source: Inyova

According to the survey, the three most important factors when investing are low costs (22%), high return (20%), and sustainability and social impact (20%).

The primary goals of the experienced investors are fairly evenly divided between three options: security for their family, enough passive income to retire early, or a comfortable retirement.

source: Inyova

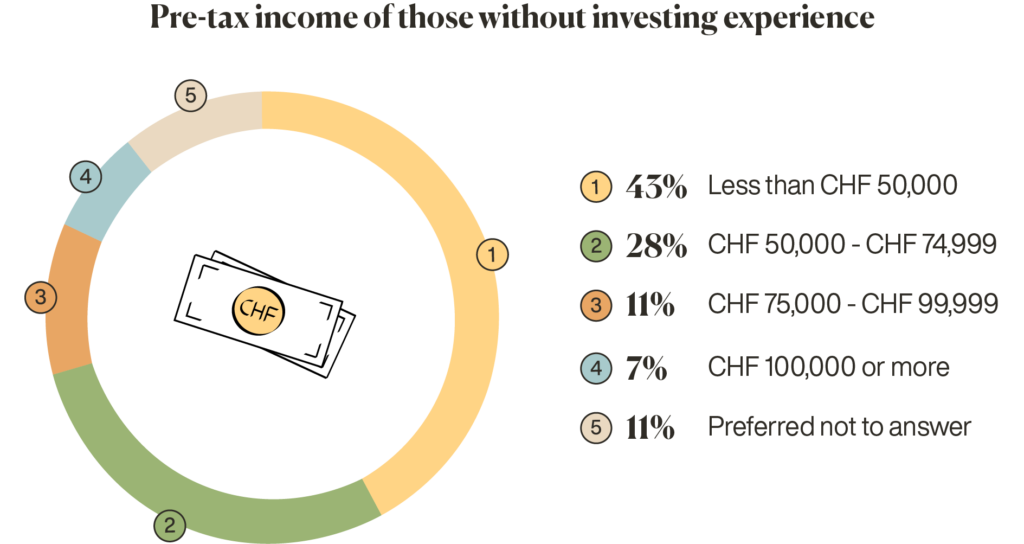

Those without investing experience

More than half of those without investing experience (55%) are aged between 18 and 29, in contrast to the experienced group, whose majority is in the 30-49 age range.

They also earn less compared with the experienced investors, and rate their confidence in their investment knowledge significantly lower. Those without investing experience rate their investment knowledge roughly 1.6 out of 5 (in comparison, those with experience rate their knowledge 3.6 out of 5 on average).

Overall, those without investing experience tend to be younger, predominantly female, and earn less.

- 43% have an annual pre-tax income below CHF 50,000

- 28% earn CHF 50,000 to 75,000

When it comes to their primary financial goal, more than half of the inexperienced investors state that they want to give their children and/or family a secure life.

source: Inyova

source: Inyova

source: Inyova

Why are demographics important?

Our survey also included questions relating to socio-economic demographics. This is an important component of any survey.

Taken at face value, the investment statistics we gathered from our initial ten questions in the survey are interesting but ultimately too vague to provide any real information on their own. That’s because demographic factors like age, gender, financial and working experience, and financial goals have a big influence on whether or not someone decides to invest, and where and how they do so.

Which demographic factors play a role in investment habits?

Age

People are often impacted by the social and political events occurring around them. A person’s age can shape their attitude towards investing, their money habits, and the investment opportunities they are attracted to.

Furthermore, how different generations choose to manage their investments varies due to exposure to and ease with developing technology. In this investment research, the majority of people surveyed were between 18 and 50 years old, with roughly 7% aged 50 or older. Our data revealed that more than half of those investing are aged between 30 and 49. This means that half of them clearly belong to the generation of the Millennials (those born between 1981 and 1995).

The defining characteristics of Millennials include their preference for being digitally connected, and their tech-savviness. More than half of those with investing experience state that they prefer to manage their own money. Given that someone who manages their own money is likely to be using an online platform to do so (and thus is fairly digitally savvy), this falls in line with the Millennials’ preferences.

Of course, we have to take into account that Millennials only make up half of our survey population. The other survey participants opt for a mixture of managing their own money and getting advice from a bank, personal or online advisor.

Gender

In the past, women were severely underrepresented as investors. And while that’s changing, previous Inyova research revealed that one in three Swiss women still feel uninformed about investing to the point where they don’t feel comfortable taking the first step.

In our survey, more participants identified as female (52.57%) than as male (46.60%). Less than 1% chose not to state their gender (0.83%).

Those who identified as female have less investment knowledge and experience than their male counterparts. While women rate their investment knowledge 2.02 out of 5, men rate theirs 3.06. The difference is even more significant when it comes to investment experience. 56% of women have never invested, as compared to 20% of men.

Finally, their primary goals differ as well. Women tend to focus on giving their children and family a secure life (47%, as compared to 29% of men), while men focus more on passive income (27%, as compared to 15% of women).

Pre-tax income

A common misconception about investing is that you have to be rich to start investing (PS — that’s not true! Check out our article on how you can start investing with small amounts). While that myth is slowly being unwrapped, it’s useful to consider the pre-tax income level of those participating in our survey.

Our data showed that 30% of those surveyed earn less than CHF 50,000 annually. Those with an income of more than CHF 100,000 per year are in second place (21.23 %), followed by two ranges between CHF 50,000 and CHF 100,000.

Those with investing experience have a higher income overall – 32% earn more than CHF 100,000, with those earning between CHF 75,000 and 99,000 coming in second (22%).

In comparison, 43% of those without investing experience earn less than CHF 50,000 per year. Those earning between CHF 50,000 and CHF 74,999 had the next highest percentage at 28%.

There are a few possible reasons for these differences. Firstly, those with more disposable income feel more comfortable using it for investments. Additionally, those who invest often make more money because their investments create compound interest.

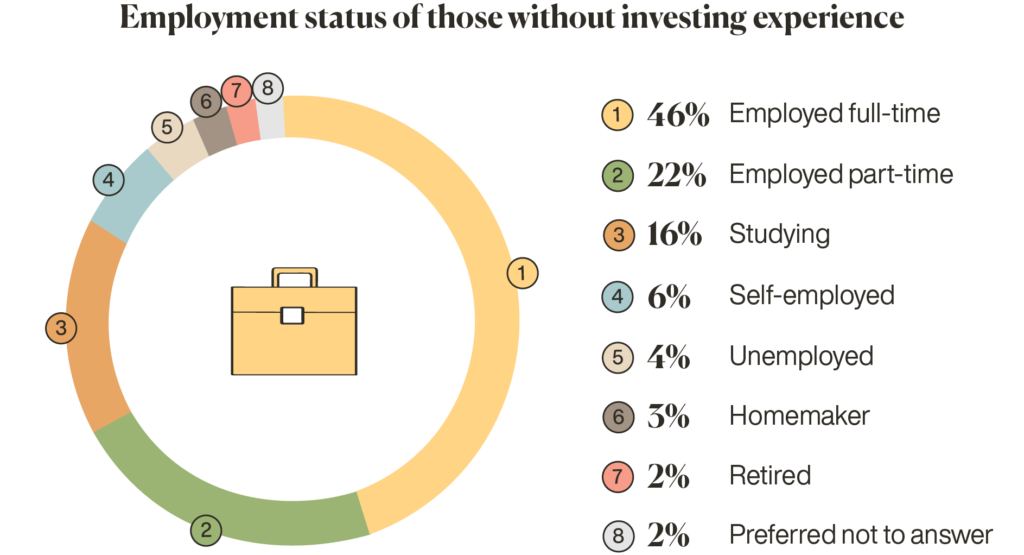

Employment status

More than half of the survey participants are employed full-time (52%), while 20% are employed part-time, and 7% are self-employed. Students comprised 13% of the survey population. A small portion identified as unemployed (2%), and less than 2% identified as a stay-at-home spouse.

In our survey, 62% of full-time employees have investing experience, as compared to 52% of part-time employees. More than half of self-employed people have experience (61%), whereas only 48% of students have investing experience.

When it comes to putting aside money each month for investments or savings, full-time employees set aside larger amounts of money. 33% set aside between CHF 500 and 1,000, with another 30% setting aside between CHF 1,000 and 5,000 per month.

In contrast, part-time employees or self-employed people set aside lower amounts — less than CHF 500. 38% of part-time employees, 41% of self-employed people and 67% of students set aside less than CHF 500.

For the most part, each group has similar investment types (‘stock market,’ ‘savings account,’ ‘Pillar 3a/retirement accounts’) — with one exception. Instead of ‘investment funds/EFT’s,’ 12% of self-employed people invest in start-ups or private equity.

It should be noted that although the investment types are similar, the groups differ in where they invest. Full-time and part-time employees are more likely to invest in Pillar 3a/retirement accounts (21% and18% respectively). By contrast, self-employed people and students primarily choose savings accounts (20%).

Working experience

Like age, working experience plays a significant role in whether or not someone invests, or how they choose to do so. Generally speaking, the longer someone’s work experience, the more familiar they are with dealing with money — regardless of whether or not that familiarity translates into positive financial habits.

Nearly half of those surveyed have 0-9 years of working experience (48%), compared with 10-19 years (32%), or 20-30 years (14%). Those with more than 31 years of work experience comprised 6% of those surveyed.

When it comes to investing experience, roughly half or more of each group have at least some. But as the years of working experience increase, so do the percentages of those who consider themselves experienced investors:

- 50% of people who have 0-9 years of work experience hold investments, but only 3% consider themselves experienced investors.

- 64% of people who have 10-19 years of work experience hold investments, and 8% consider themselves experienced investors.

- 60% of people who have 20-30 years of work experience hold investments, and 11% consider themselves experienced investors.

Our survey also revealed a surprising trend regarding how much money people set aside for investments each month. Those who have less work experience tend to set aside more — 37% of those with 0-9 years of work experience set aside between CHF 500 and 1,000 monthly. In comparison, 34% of those with 10-19 years of work experience set aside less than CHF 500. Once work experience crosses the 20-year mark, the percentage rises again — 40% set aside less than CHF 500.

The same trend persists when it comes to adding money to investments. 90% of those with 0-9 years of work experience state that they plan to add money within this year. 87% of those with 10-19 years of work experience plan to do the same, and the percentage drops to 70% when it comes to those with 20-30 years of work experience.

It’s great to see people investing more money earlier on in their careers – since these early deposits benefit the most from compound interest.

Primary financial goal

Ultimately, the number one financial goal of the survey participants was ‘to give my children/family a secure life’. They’re not alone in that desire. Part of Inyova’s mission is to create a more sustainably secure world through investing. And it starts from the top — check out Inyova CEO Dr. Tillman Lang’s TEDx Talk on why he invests.

Retirement and generating passive income also feature heavily. 20% identify their primary financial goal as ‘to create enough passive income to retire early,’ and 17% claim ‘a comfortable retirement’ as theirs.

With only a small portion of the survey population in the 50-70 years age range (7%), it’s heartening to note the focus on retirement. It’s great to see that younger generations recognise the importance of planning for retirement.

The focus on passive income is also noteworthy, especially when compared to the other primary financial goals. Although rental properties are considered a ‘traditional’ form of passive income, only 9% of those surveyed claim ‘to own a home’ as a primary financial goal.

source: Inyova

source: Inyova

Conclusions

This survey is one of the biggest pieces of research on Swiss investment habits to date, with 603 people surveyed in total. Based on this data, we can draw a few key conclusions about how investment habits are changing and what we may observe in future investment statistics.

First, there’s a clear trend towards planning on investing more money within the upcoming twelve months — 87% of experienced investors state that they would. Because of this, there may be more demand for opportunities that match investor priorities: low cost, high return, and a focus on sustainability and social impact.

(Here’s how impact investing meets that demand)

Secondly, there’s significant investment potential for females between the ages of 18 and 29. As our survey showcased, this group has the least experience and income but a strong desire to create a secure future. As they approach their peak earning years (generally mid to late 30s), they’ll likely have extra income to put towards investing.

Finally, due to the continued intersection of technology and finances, it’s likely that investors will continue to seek a blended way of managing their money — making use of an online and/or personal advisor, with some DIY on the side.

With this in mind, all investors — experienced or not — will need access to straightforward, clear information on investing research and opportunities. They’ll want to be aware of things like hidden costs, which many providers hide in entry and exit fees, transaction fees, performance fees, fund fees, and more.

Investing for the future

At Inyova, we’re committed to offering investments that promote a cleaner, fairer world. We stand for transparency — both in terms of our simple fee, as well as the exact companies that you invest in through your personal Inyova portfolio.

Whether your personal financial goal is to create a secure future for your family or retire early, if you’re curious about using impact investing to do so, we’d love to chat. You can also click here to create your free investment strategy and get started today!